Business line of credit vs loan for bicycle inventory – When it comes to financing bicycle inventory, business owners have two main options: a business line of credit or a loan. Both options have their own advantages and disadvantages, so it’s important to understand the differences before making a decision.

In this article, we’ll compare and contrast business lines of credit and loans, and discuss the factors that bicycle retailers should consider when choosing between the two.

Types of Business Financing

Bicycle retailers have various financing options to support their inventory needs. These options differ in terms of repayment structure, interest rates, and collateral requirements.

The primary types of business financing for bicycle inventory include lines of credit, loans, and equity investments.

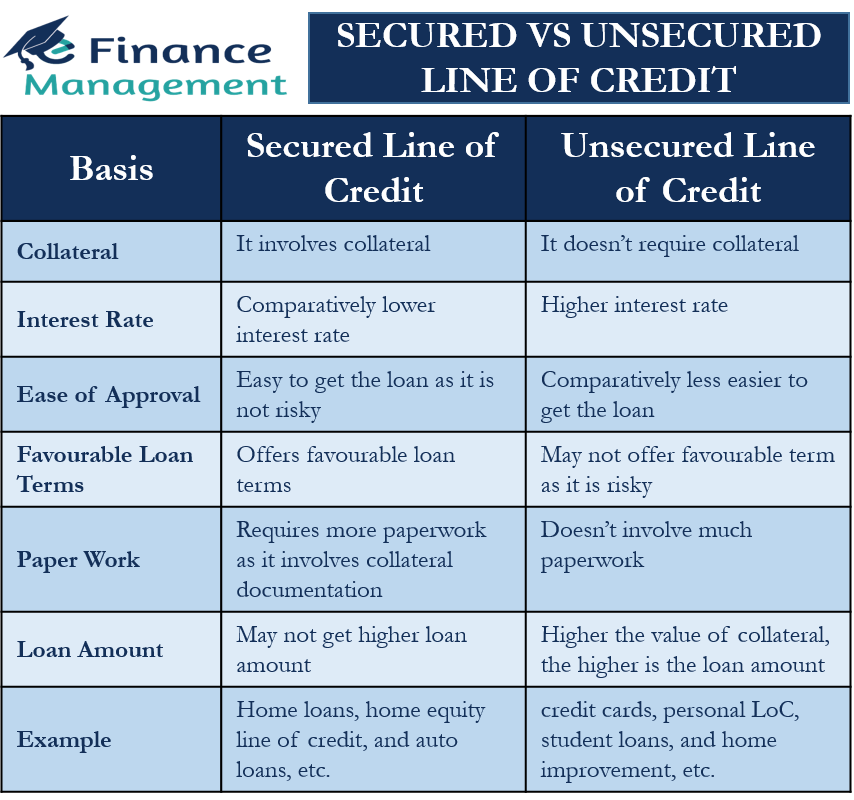

Lines of Credit

A line of credit is a revolving loan that allows businesses to borrow funds up to a pre-approved limit. This type of financing provides flexibility as businesses can draw on the line of credit as needed and repay it over time.

- Advantages: Flexible access to funds, lower interest rates than loans.

- Disadvantages: Potential for high fees, requires good credit history.

Loans

Loans are lump-sum financing options with fixed repayment terms and interest rates. Businesses receive the loan amount upfront and make regular payments until the loan is fully repaid.

- Advantages: Predictable repayment schedule, lower interest rates for secured loans.

- Disadvantages: Limited access to funds, can be difficult to qualify for.

Equity Investments

Equity investments involve selling a portion of the business’s ownership to investors in exchange for capital. This type of financing provides long-term funding but dilutes the owner’s equity stake.

- Advantages: No repayment obligation, potential for higher returns.

- Disadvantages: Loss of ownership control, can be expensive.

Business Line of Credit vs. Loan

When it comes to financing bicycle inventory, there are two main options: a business line of credit and a loan. Both options have their own advantages and disadvantages, so it’s important to understand the differences before making a decision.

A business line of credit is a revolving line of credit that allows you to borrow money up to a certain limit. You can draw on the line of credit as needed, and you only pay interest on the amount of money you borrow.

This can be a good option if you need flexibility in your financing, as you can borrow more or less money as needed.

A loan, on the other hand, is a one-time loan that you repay over a fixed period of time. The interest rate on a loan is usually fixed, and you will make monthly payments until the loan is paid off.

This can be a good option if you need a specific amount of money and you want to know exactly how much you will pay each month.

Advantages and Disadvantages of Business Lines of Credit

- Advantages:

- Flexibility: You can borrow money as needed, and you only pay interest on the amount you borrow.

- Convenience: Business lines of credit are easy to apply for and can be approved quickly.

- Lower interest rates: Business lines of credit often have lower interest rates than loans.

- Disadvantages:

- Variable interest rates: The interest rate on a business line of credit can fluctuate, which can make it difficult to budget.

- Personal guarantee: Many business lines of credit require a personal guarantee, which means that you are personally liable for the debt if your business defaults.

Advantages and Disadvantages of Loans

- Advantages:

- Fixed interest rates: The interest rate on a loan is fixed, which means that you will know exactly how much you will pay each month.

- Predictability: Loans have a fixed repayment schedule, which can make it easier to budget.

- No personal guarantee: Loans do not typically require a personal guarantee, which means that you are not personally liable for the debt if your business defaults.

- Disadvantages:

- Less flexibility: Loans are not as flexible as business lines of credit, and you cannot borrow more money once the loan is approved.

- Higher interest rates: Loans often have higher interest rates than business lines of credit.

- Longer approval process: Loans can take longer to apply for and be approved than business lines of credit.

Specific Examples

Here are some specific examples of how a business line of credit and a loan can be used to finance bicycle inventory:

- Business line of credit:A business line of credit can be used to finance the purchase of a large order of bicycles, or to cover unexpected expenses such as a sudden increase in demand.

- Loan:A loan can be used to purchase a new fleet of bicycles for a rental business, or to finance the construction of a new bike shop.

Factors to Consider When Choosing Financing

:max_bytes(150000):strip_icc()/Basics-lines-credit_final-0c20f42ed1624c349604fdcde81da91c.png)

Bicycle retailers must carefully consider several factors when selecting between a business line of credit and a loan to optimize their financing strategy. These factors include the retailer’s creditworthiness, the amount of financing required, and the repayment terms.

The retailer’s creditworthiness plays a crucial role in determining the availability and terms of both financing options. A strong credit history and score can qualify the retailer for lower interest rates and more favorable repayment terms, making a business line of credit or loan more affordable.

Amount of Financing Needed

The amount of financing required is another key consideration. A business line of credit provides flexibility by allowing the retailer to access funds as needed, up to a pre-approved limit. This flexibility can be beneficial for retailers with fluctuating inventory needs or seasonal sales patterns.

In contrast, a loan provides a fixed amount of financing that must be repaid according to a set schedule. This option may be more suitable for retailers with a specific, one-time financing need, such as purchasing new inventory or expanding their operations.

Repayment Terms, Business line of credit vs loan for bicycle inventory

The repayment terms of the financing option should also be carefully evaluated. A business line of credit typically has shorter repayment terms than a loan, with interest charged only on the amount of credit used. This can result in lower overall interest costs for retailers who do not need to access the full line of credit for an extended period.

Loans, on the other hand, have fixed repayment schedules and interest rates. The retailer must make regular payments, regardless of whether the full amount of the loan has been used. This can result in higher overall interest costs if the retailer does not fully utilize the loan proceeds.

Application Process

The application process for a business line of credit or loan typically involves several steps:

1. Complete an application form:This form will ask for basic information about your business, such as your name, address, and financial history.

2. Provide supporting documentation:This may include financial statements, tax returns, and business plans.

3. Meet with a loan officer:The loan officer will review your application and supporting documentation and ask you questions about your business.

4. Get approved for financing:If the loan officer approves your application, you will receive a loan agreement that Artikels the terms of the loan.

Tips for Increasing the Chances of Approval

- Have a strong credit history:Lenders will look at your credit history to assess your risk. A good credit score will increase your chances of getting approved for a loan with a favorable interest rate.

- Provide a detailed business plan:A well-written business plan will show the lender that you have a clear understanding of your business and its financial goals.

- Have a strong financial track record:Lenders will want to see that your business has a history of profitability and financial stability.

- Be prepared to answer questions:The loan officer will ask you questions about your business and its financial performance. Be prepared to answer these questions honestly and thoroughly.

Best Practices for Managing Financing: Business Line Of Credit Vs Loan For Bicycle Inventory

:max_bytes(150000):strip_icc()/dotdash_Final_Line_of_Credit_LOC_May_2020-01-b6dd7853664d4c03bde6b16adc22f806.jpg "Credit revolving debt line installment student vs choosing banks professional big examples loan loans source")

Managing business lines of credit and loans effectively is crucial for optimizing bicycle inventory management. Here are some best practices to consider:

Monitor and Forecast Cash Flow

Regularly track income and expenses to anticipate cash flow needs. This helps avoid over-borrowing or missing payments, ensuring financial stability.

Use Lines of Credit Flexibly

Business lines of credit offer flexibility to draw funds as needed, without the commitment of a loan. Use this option for short-term expenses or seasonal fluctuations in inventory demand.

Negotiate Favorable Terms

Negotiate competitive interest rates, repayment schedules, and fees when obtaining financing. Explore multiple lenders to compare offers and secure the best terms for your business.

Maintain Good Credit

Maintain a strong credit history by making timely payments and managing debt responsibly. This improves access to financing and secures lower interest rates.

Monitor Inventory Levels

Keep track of inventory levels to avoid overstocking or understocking. Adjust financing amounts as needed to align with inventory requirements.

Ultimate Conclusion

Ultimately, the best way to decide which type of financing is right for your business is to speak with a financial advisor. They can help you assess your needs and make the best decision for your business.

FAQ Guide

What is a business line of credit?

A business line of credit is a revolving loan that allows businesses to borrow money up to a certain limit. The interest rate on a business line of credit is typically variable, and the payments are usually made monthly.

What is a loan?

A loan is a lump sum of money that is borrowed from a lender and repaid over a period of time. The interest rate on a loan is typically fixed, and the payments are usually made monthly.

Which is better for bicycle inventory, a business line of credit or a loan?

The best option for financing bicycle inventory depends on the specific needs of the business. A business line of credit may be a better option if the business needs to borrow money on a short-term basis, while a loan may be a better option if the business needs to borrow a large amount of money over a longer period of time.